What is Nationwide Indexed Principal Protection?

NW-IPP is a group fixed indexed annuity for retirement plans that tracks the performance of the S&P 500® Daily Risk Control 5% Excess Return Index (Index). Your money is not directly invested in the Index, but its performance is used to credit you with interest earnings, subject to a specific limit, called a "cap rate".

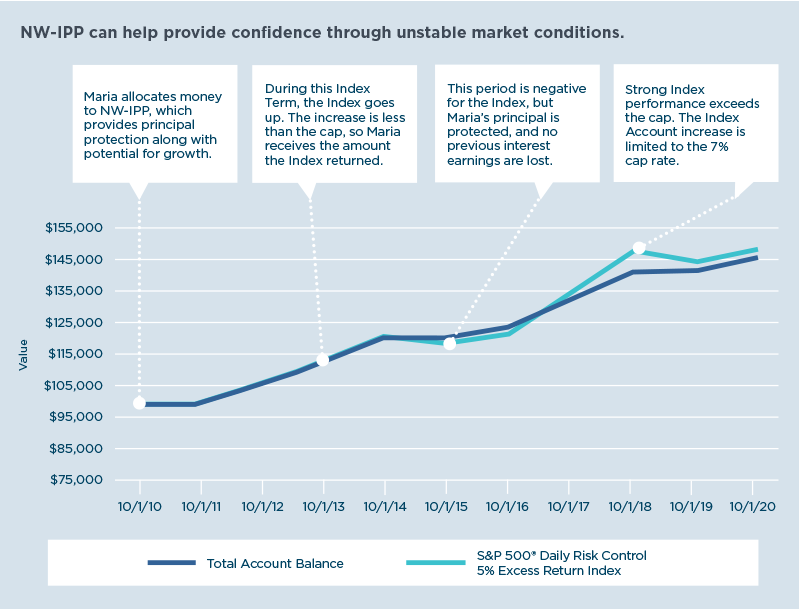

- If the Index goes up, your account will be credited with interest earnings up to the cap rate. For example, if the Index gains 8% at the end of the Index Term and your cap rate is 7%, contributions to this account will be 7% interest earnings.

- If the Index goes down, your account loses nothing because your principal is protected.

Hypothetical assumptions: A $100,000 one-time contribution is allocated to Nationwide Indexed Principal Protection℠ with a 5-year book value payout term. This chart demonstrates historical performance of S&P 500® Daily Risk Control 5% Excess Return Index assuming a 7% cap and a 0% floor. This example assumes that the initial deposit on 10/1/2010 remains invested in NW-IPP for 10 years, and the cap remains the same over the illustrated 10 years. The cap and interest rate may be changed for each term. This illustration is not a projection or prediction of future performance. The performance could be significantly different than the investment performance shown and shouldn’t be considered a representation of performance or investor experience of the index(es) in the future. Withdrawals will reduce the contract value; this illustration does not demonstrate the impact of withdrawals.

Potential benefits of NW-IPP:

- Principal investment protection from market declines

- Growth potential when markets are increasing, subject to the cap rate

- Gains are locked in and become part of the principal at Index Term renewal

- Two contribution options: payroll deductions or a lump-sum dollar amount exchanged from another investment option in your plan (no minimum required)

- If you should change your mind, you can exchange your money out of this investment option (restrictions may apply)

- A simple web experience makes choosing this investment option easy

Case study 1: Exchange In

1. At any time, Maria can exchange any dollar amount from another investment option in her retirement plan.

2. Money allocated to NW-IPP goes into an Interest Account that earns daily interest until the end of the current quarter.

3. At the beginning of the next calendar quarter, money sitting in the Interest Account is swept into an Index Account for one year.

4. Interest earnings are credited to the Index Account at the end of the one-year Index Term and depend on the return of the Index, subject to the cap rate.

5. The one-year Index Term automatically renews with a new cap rate. Any interest earnings are locked in and the new principal amount is protected for the following year.

* Principal + Interest earnings will become principal at the beginning of the next Index Term.

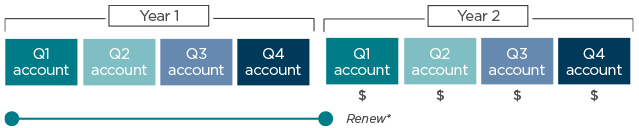

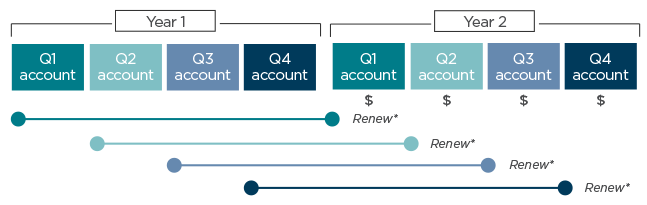

Case study 2: Payroll Deduction

1. Every pay cycle, money is deducted from Craig’s paycheck and contributed to his retirement plan account.

2. The money is then invested according to his allocations. Up to 100% of a portfolio can be allocated to NW-IPP.

3. Money allocated to NW-IPP goes into an Interest Account that earns daily interest until the end of the current quarter.

4. At the beginning of each quarter, money sitting in the Interest Account is swept into a new Index Account for one year. It’s possible to have up to four Index Accounts at any given time.

5. Interest earnings are credited to each Index Account at the end of the one-year Index Term and depend on the return of the Index, subject to the cap rate.

6. Each one-year Index Term automatically renews with a new cap rate. Any interest earnings are locked in and the new principal amount is protected for the following year.

* Principal + Interest earnings will become principal at the beginning of the next Index Term.